LexiFi Apropos reduces what was once a matter of hours in a few seconds.

The Value at Risk (VaR) and conditional VaR (CVaR) are two important risk measures for quantifying and managing both product and portfolio risk. In LexiFi’s Software, we put your at disposal two methodologies to calculate these: the Historical Scenarios and the Monte Carlo scenario generation method.

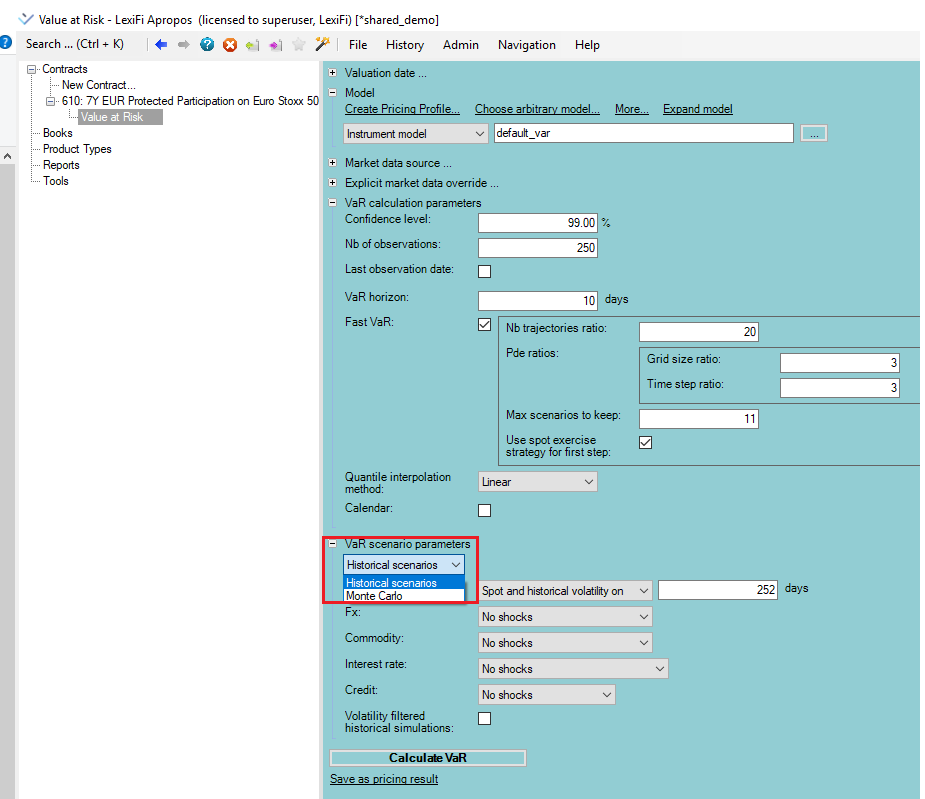

Figure 1: Value at Risk scenario parameters

Contracts are priced using a number of different scenarios where each scenario modifies the current market data for the contract underlying spots and volatilities by applying shocks inferred from observed market changes. Volatility shocks are applied to all volatility data (constant volatilities, term-structured curves and smiled surfaces). Value at Risk, Tail-VaR, P&L distribution and details on scenarios are available for inspection. The generated distribution of P&L vs shocks can be viewed both graphically and in charts.

Use the Fast-VaR mode to drastically speedup calculations on a portfolio of contracts by iteratively selecting computation scenarios that will be needed.

Video 1: Computing VaR for a contract

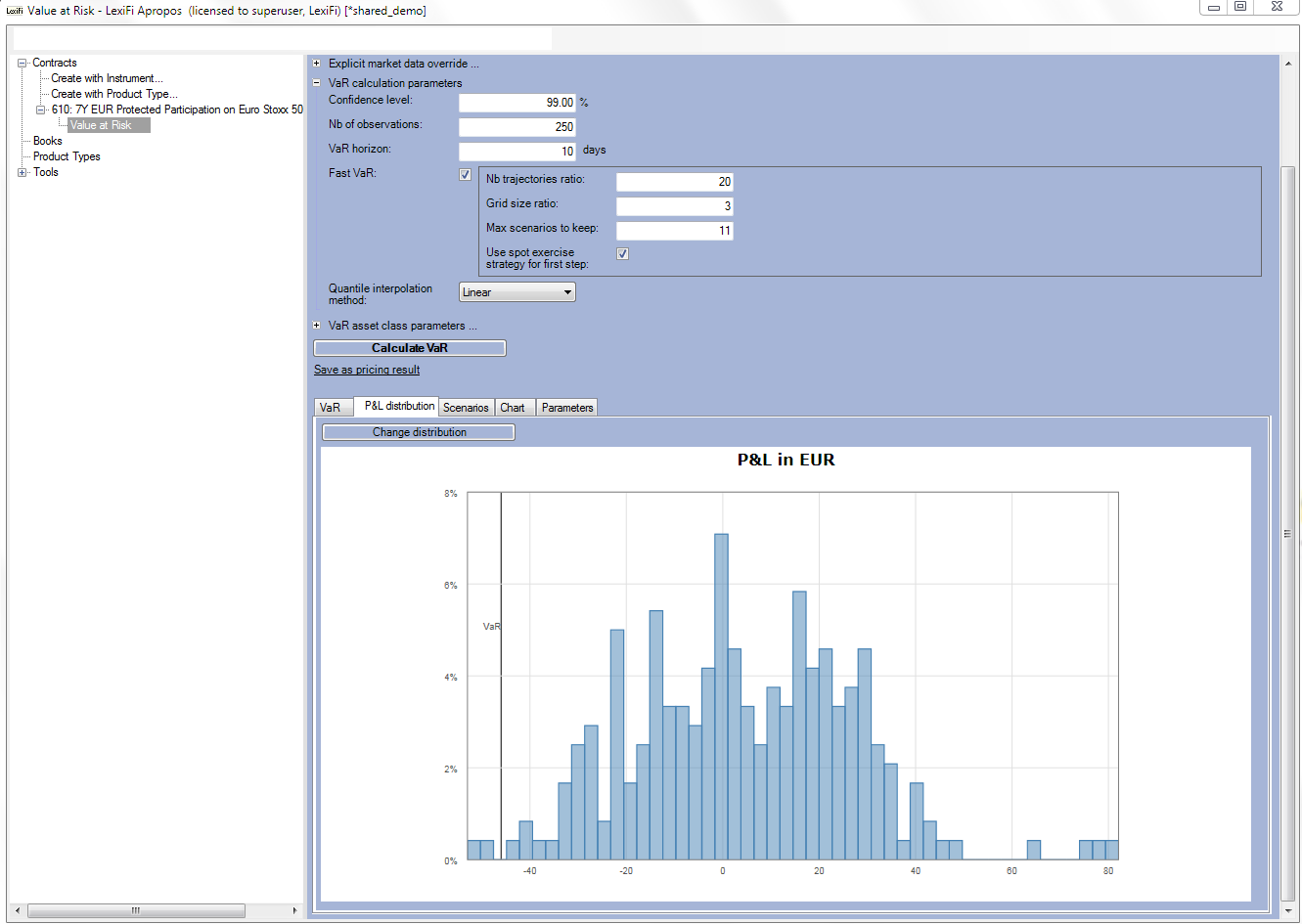

Figure 2: Value at Risk analysis and P&L graph

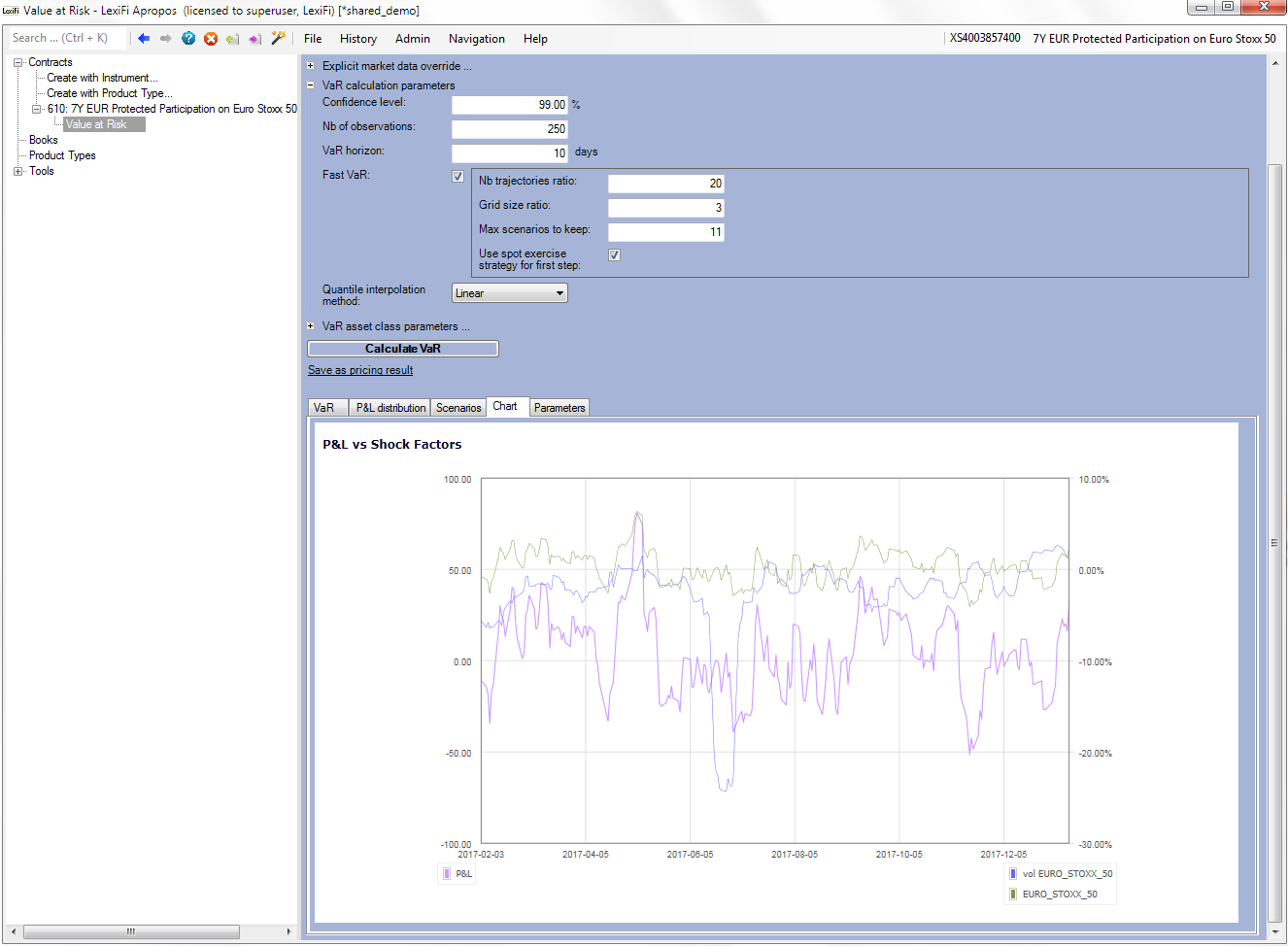

Figure 3: Value at Risk analysis and P&L vs shock factors chart

Video 2: Computing VaR on positions

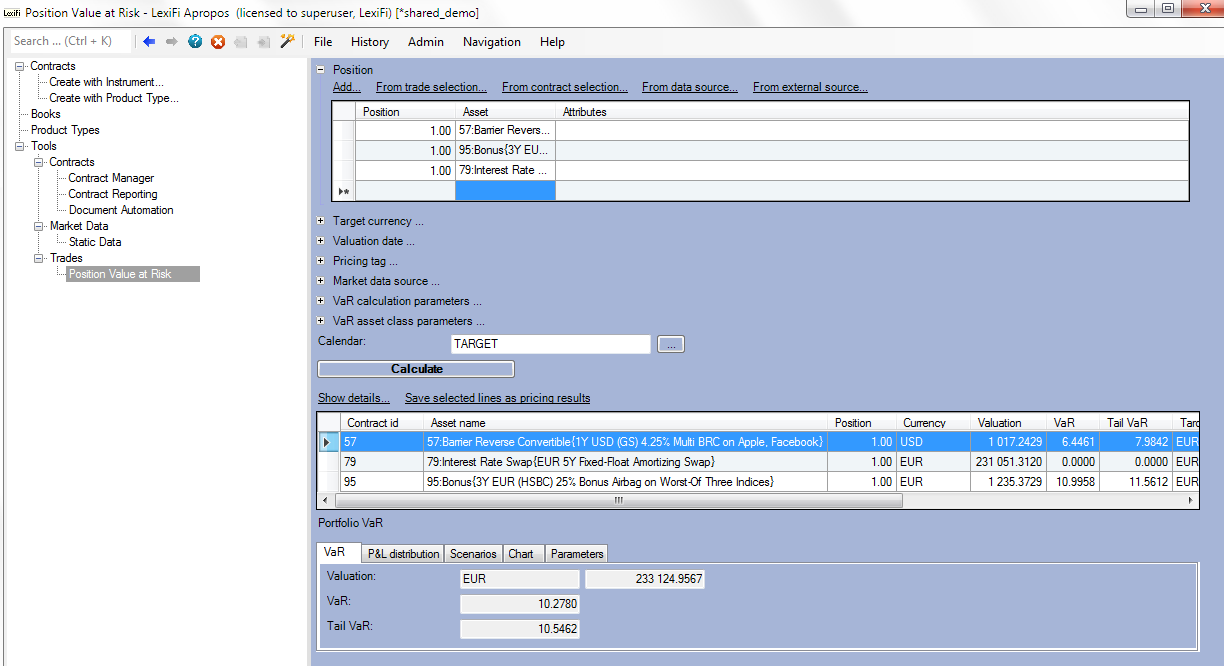

Figure 4: Position Value at Risk analysis